Surcharge Payment Processing:

How to Reduce Credit Card Fees While Staying Compliant

Credit card processing fees are a growing concern for small business owners, especially as more customers choose the convenience of plastic over cash. Whether you run an auto shop, a retail store, or a service-based business, the cost of accepting credit cards can quickly eat into your profits.

That’s why more and more businesses across the country are turning to surcharge payment processing as a smart, compliant way to offset these rising expenses.

At iSmart Payments, we help business owners implement surcharge programs that eliminate credit card fees, boost profit margins, and maintain transparency with customers. In this comprehensive guide, you’ll learn what surcharge payment processing is, how it compares to convenience fees and service charges, and how to legally and effectively implement a solution that works for your business.

What Is Surcharge Payment Processing?

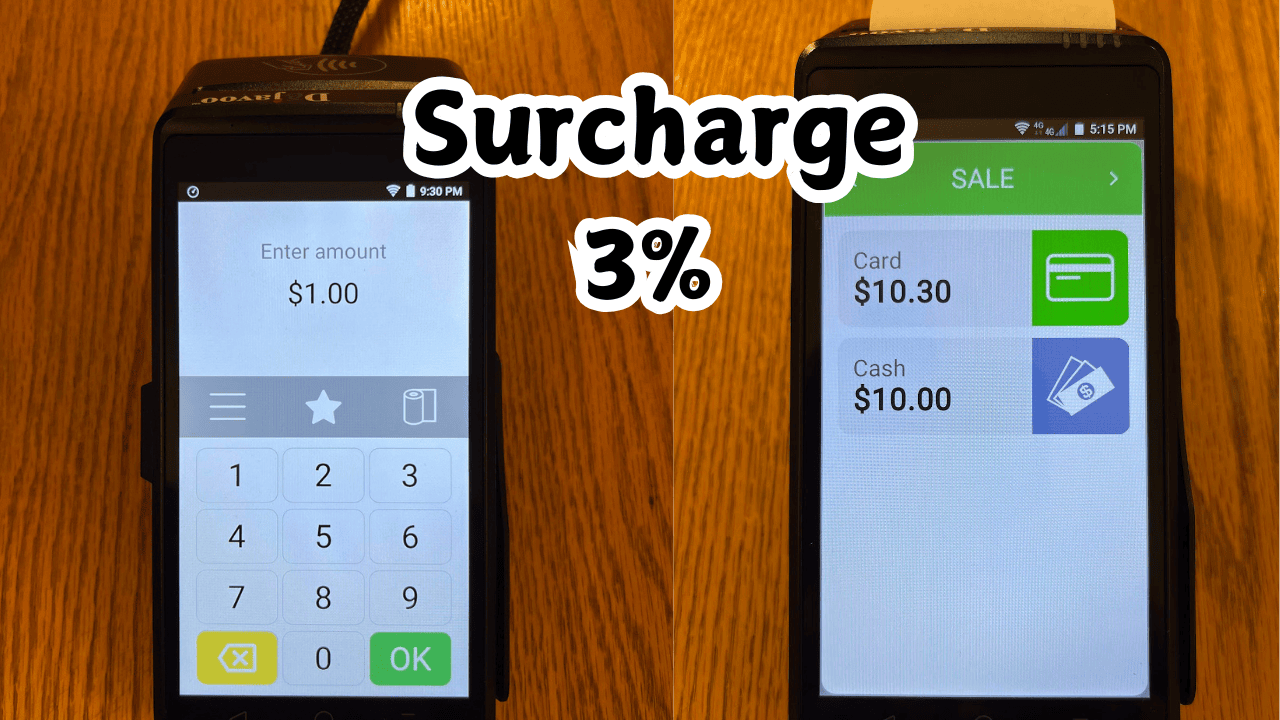

Surcharge payment processing is a method that allows businesses to add a small 3% fee to transactions paid with a credit card. This surcharge helps cover the cost of card processing, shifting the expense from the business owner to the cardholder.

This model allows businesses to:

- Avoid absorbing costly processing fees.

- Keep listed prices consistent for all customers.

- Encourage cash payments.

- Improve profit margins without raising overall pricing.

Surcharge Will Save Your Business:

Based on a 4% Rate Savings…

| Mo Card Volume: | Mo Savings | 1 Year Savings | 5 Year Savings |

|---|---|---|---|

| $5,000 | $200 | $2,400 | $12,000 |

| $10,000 | $400 | $4,800 | $24,000 |

| $20,000 | $800 | $9,600 | $48,000 |

| $50,000 | $2,000 | $24,000 | $120,000 |

| $100,000 | $4,000 | $48,000 | $240,000 |

| $250,000 | $10,000 | $120,000 | $600,000 |

Why Businesses Are Turning to Surcharge Payment Processing

For years, business owners have silently absorbed credit card processing fees, considering them a “cost of doing business.” But with more purchases happening via card—especially online or via mobile—these fees add up quickly.

Here’s why surcharge payment processing is gaining traction:

- Protects Your Margins: Instead of losing 3% or more per transaction, you retain your revenue.

- Transparent for Customers: Customers see the cost of using a card upfront and can choose to pay cash instead.

- Legal in Most States: With proper setup and disclosure, surcharging is fully legal in most U.S. states.

- Easy Implementation: With providers like iSmart Payments, the setup is fast, compliant, and worry-free.

How It Works: A Real-World Example

Let’s say you own an auto repair shop, and your customer’s bill is $500.

- Under traditional payment processing, a credit card transaction may cost you 3%, or $15.

- With surcharge payment processing, you charge $515 to the customer.

- You keep the full $500, and the $15 covers the processing fee.

The next day, $500 is deposited into your account. You’ve saved money, and the customer was clearly informed of the additional cost upfront.

Surcharge VS Dual Pricing

Legal Requirements for Surcharge Payment Processing

To legally implement a surcharge model, your business must follow specific rules set by card brands and state regulations:

✅ Card Brand Guidelines (we implement):

- According to Visa’s surcharge rules, merchants must notify Visa in advance and clearly disclose surcharges to customers. However as of April 2023 it is no longer required.

- Surcharges can only be applied to credit card transactions, not debit or prepaid cards. Our card terminal identifies all debit cards (based on the bank BIN) and removes the fee no matter if it’s run through the PIN Debit network or credit network. When a merchant is set up for surcharging, the business will pay for the fees for the specific cards that do not allow surcharging. FYI, debit cards cost less than .5% to process.

- The surcharge must not exceed the actual cost of acceptance (capped at 3%–4% depending on provider).

✅ Customer Disclosure:

- Clear signage at the point of entry and sale is required.

- The terminal must display the surcharge amount during the transaction.

- Receipts should show the surcharge as a separate line item.

✅ State Laws:

Surcharging is currently not allowed in Connecticut, Massachusetts, New York, Maine, and Puerto Rico. In all other states, it’s legal with proper compliance. If your business is in one of these states consider Dual Pricing we offer instead.

iSmart Payments handles all of this above for you, ensuring that your business is fully compliant from day one.

Transparency in pricing is critical—not just for customer trust but for compliance. The FTC emphasizes truth in advertising as a key standard for businesses.

Surcharge Payment Processing vs. Convenience Fee vs. Service Charge

Though similar in appearance, surcharges, convenience fees, and service charges are not the same. Each has its own rules, use cases, and restrictions.

💳 Surcharge

- What it is: A fee added to credit card payments only.

- Used for: Recouping card processing costs.

- Limitations: Not allowed on debit or prepaid cards; capped at 3%.

📲 Convenience Fee

- What it is: A flat fee charged for using a non-standard payment method (e.g., paying online vs. in person).

- Used for: Offering an alternative or convenient way to pay.

- Limitations: Must be a fixed amount; not based on payment method alone.

🧾 Service Charge

- What it is: A broader fee added for services provided (e.g., delivery, handling, or administrative fees).

- Used for: Covering non-payment related costs.

- Limitations: Can apply to any payment method but must be clearly disclosed.

How iSmart Payments Simplifies the Process

We understand that many business owners want to save money—but don’t have time to research complex compliance rules or learn new systems. That’s where we come in.

When you choose iSmart Payments for your surcharge payment processing, you get:

✅ Free Surcharge-Ready Terminal – Preprogrammed to display the increased (3-4%) price or optional, showing both cash and credit prices with the latter being dual pricing

✅ Full Compliance Setup – We handle notifications, signage, disclosures, and card brand rules

✅ Transparent Pricing – Just $10/month for “credit cards” processing—no hidden fees

✅ Next-Day Funding – Keep your cash flow moving fast

✅ No Long-Term Contracts – Month-to-month service so you stay in control

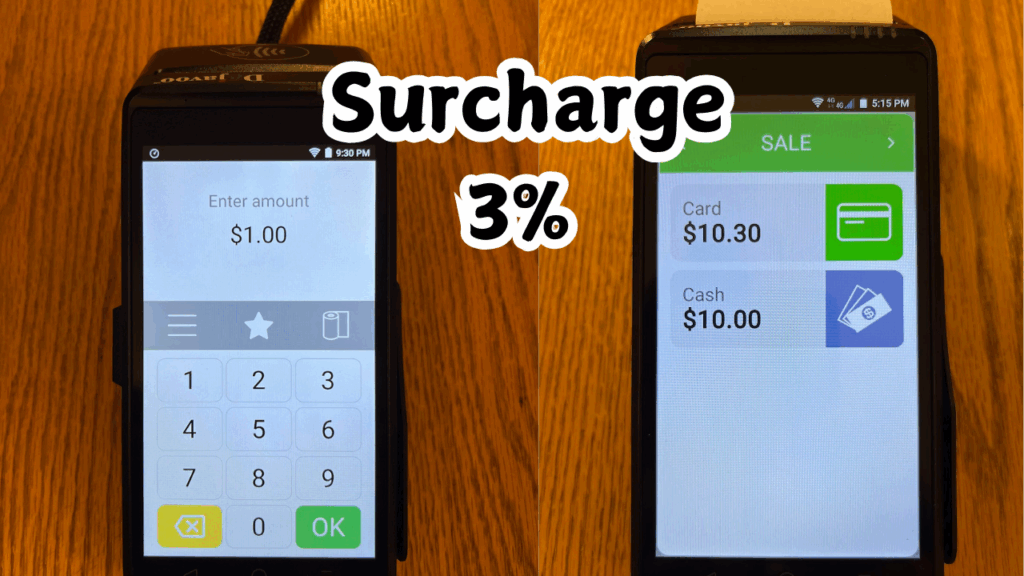

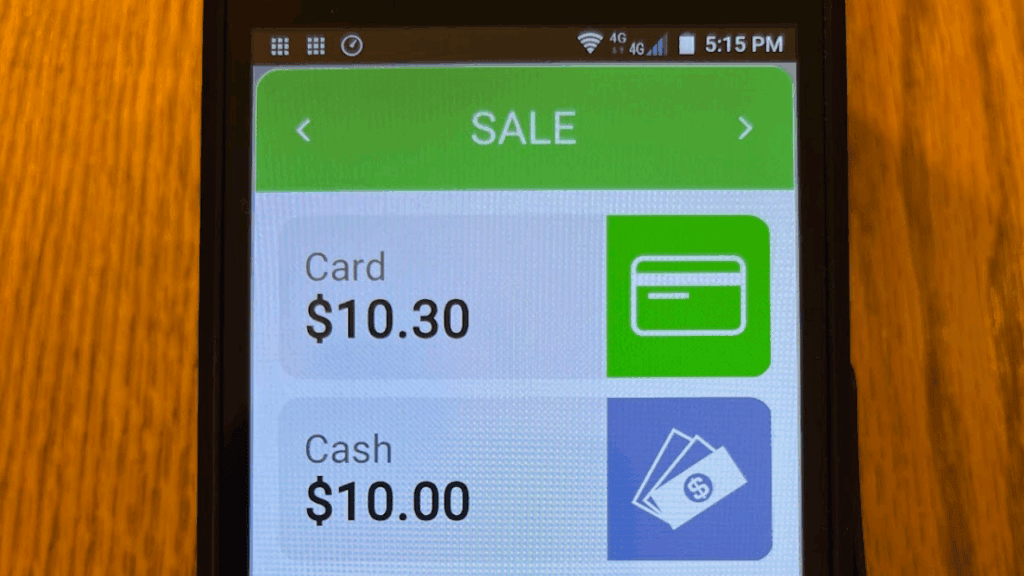

What Customers Will See

When a customer pays using a credit card, they’ll see something like:

- Subtotal: $100.00

- Surcharge (3%): $3.00

- Total: $103.00

If they choose to pay with cash or debit, they’ll simply pay the $100. This level of clarity builds trust and gives customers the power to choose.

Dual Pricing: Another Transparent Option

If you’re in a state that prohibits surcharging—or you prefer a pricing model that doesn’t separate out the surcharge line—you might consider dual pricing instead.

In a dual pricing system, the terminal shows two totals:

- Cash Price: $100

- Card Price: $103

This is a clean, compliant model that’s growing in popularity, especially in retail and automotive sectors. Many gas stations already use this model, and customers are familiar with the format. We offer this without PCI compliance fees.

- Free

Terminals

- No Contract

- Next A.M. Funding

How iSmart Payments Simplifies the Process

Q: Is it legal to add a surcharge for credit card customer payments?

Yes, in most states—when implemented correctly. We ensure your setup complies with card network rules and local laws.

Q: Will customers be upset?

Some may ask questions, but most customers appreciate transparency. When presented properly, surcharging or surcharge payment processing is rarely a dealbreaker.

Q: What’s the difference between a surcharge and a convenience fee?

A surcharge is applied specifically for using a credit card, while a convenience fee is for using an alternative payment channel (e.g., online or phone).

Q: How much can I charge?

Surcharges are typically capped at 3% (Visa) (some providers MC allow up to 4%). You cannot profit from the surcharge—it can only cover your actual processing costs.

Real Results from Real Businesses

Here’s how one auto shop benefited from switching to surcharge payment processing with iSmart Payments:

- Before: Processing $40,000/month with 3.5% average fee = $1,400/month in fees

- After: Added a 3% surcharge; customers now pay that fee

- Net Savings: $16,800/year back in the owner’s pocket

And the best part? Their customers stayed loyal—because they appreciated the upfront communication and fair pricing.

How iSmart Payments Simplifies the Process

| Benefit | Traditional Model | Surcharge Model |

|---|---|---|

| Processing Fees | Paid by business | Covered by customer |

| Pricing Transparency | Low | High |

| Customer Choice | Limited | Enhanced |

| Profit Margin Protection | Poor | Strong |

| Compliance & Simplicity | Varies | Streamlined with iSmart Payments |

Take Control of Your Credit Card Fees Today

With surcharge payment processing, you no longer have to absorb the high cost of credit card acceptance. Whether you run an auto shop, a contractor business, or a retail store, iSmart Payments offers the tools and support you need to:

- Stay compliant

- Save money

- Keep your customers informed and satisfied

Ready to see how much you could save?

Contact Greg G. Kapitan at 801-205-1955 or fill out the from below to get started with a free consultation. iSmart Payments is here to help!